UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 0-14948

Fiserv, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Wisconsin | 39-1506125 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

255 Fiserv Dr., Brookfield, WI 53045

(Address of Principal Executive Offices, Including Zip Code)

Registrant’s telephone number, including area code: (262) 879-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer þ Accelerated Filer ¨ Non-Accelerated Filer ¨ Smaller Reporting Company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the common stock of the registrant held by non-affiliates as of June 30, 2008 (the last trading day of the second fiscal quarter) was $7,275,841,671 based on a closing price of $45.37 on the Nasdaq stock market on that date. The number of shares of the registrant’s common stock, $0.01 par value per share, outstanding at February 25, 2009 was 156,000,417.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this report incorporates information by reference to the registrant’s proxy statement for its 2009 annual meeting of shareholders, which proxy statement will be filed with the Securities and Exchange Commission no later than 120 days after the close of the fiscal year ended December 31, 2008.

TABLE OF CONTENTS

i

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. Forward-looking statements include those that express a plan, belief, expectation, estimation, anticipation, intent, contingency, future development or similar expression, and can generally be identified as forward-looking because they include words such as “believes,” “anticipates,” “expects,” “could,” “should” or words of similar meaning. Statements that describe our objectives or goals are also forward-looking statements. The forward-looking statements in this report involve significant risks and uncertainties, and a number of factors, both foreseen and unforeseen, could cause actual results to differ materially from our current expectations. The factors that may affect our results include, among others: the impact on our business of the current state of the economy, including the risk of reduction in revenue resulting from the elimination of existing or potential clients due to consolidation or financial failures in the financial services industry or from decreased spending on the products and services we offer; our ability to complete, and the timing of and the proceeds from, the sale of the remainder of the Fiserv ISS business, including the risk that the conditions to the completion of the transaction may not be satisfied or the required regulatory approvals may not be obtained timely or at all; our ability to successfully integrate CheckFree’s operations; changes in client demand for our products or services; pricing or other actions by competitors; the potential impact of our Fiserv 2.0 initiatives; our ability to comply with government regulations, including privacy regulations; and other factors discussed in this report under the heading “Risk Factors.” We urge you to consider these factors carefully in evaluating forward-looking statements and caution you not to place undue reliance upon forward-looking statements, which speak only as of the date of this report. We undertake no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this report.

PART I

In this report, all references to “we,” “us,” and “our” refer to Fiserv, Inc., a Wisconsin corporation, and, unless the context otherwise requires, its consolidated subsidiaries.

Overview

We provide integrated information management and electronic commerce systems and services, including transaction processing, electronic bill payment and presentment, business process outsourcing, document distribution services, and software and systems solutions. We serve approximately 16,000 clients worldwide, including banks and thrifts, credit unions, savings institutions, retailers and merchants, leasing companies, lenders, government agencies, and publicly and privately owned companies. We operate centers in the United States for full-service financial data processing, software system development, item processing and check imaging, technology support and related businesses. Our operations are principally located in the United States. In 2008, our international operations contributed approximately 5% of total revenues from Argentina, Australia, Canada, China, Colombia, Costa Rica, France, India, Indonesia, Luxembourg, Malaysia, Mexico, the Netherlands, the Philippines, Puerto Rico, Poland, Singapore and the United Kingdom.

We were formed through the combination of two major regional data processing firms that began as the data processing operations of their parent financial institutions. Since we began, we have grown by developing highly specialized services and product enhancements, adding new clients, and acquiring businesses that complement ours. We originally incorporated in Delaware in 1984, and reincorporated as a Wisconsin corporation in 1992. Our headquarters are located at 255 Fiserv Drive, Brookfield, Wisconsin 53045, and our telephone number is (262) 879-5000.

1

The Markets We Serve

General

We believe that the growing volume and types of transactions and payment mechanisms have increased the data processing and other service needs of financial institutions, and we believe that these institutions will continue to require: significant commitments of capital and human resources for information systems requirements; application of more specialized systems; and development, maintenance and enhancement of applications software. In addition, the financial industry regularly introduces and implements new lending, investment, deposit, payment and risk management products, and the distinctions among financial services traditionally offered by banking, thrift and credit union organizations continue to narrow as different types of entities seek to serve the same ultimate customers. We believe that economies of scale in data processing operations are essential to justify the required level of expenditures and commitment of human resources.

The number of financial institutions in the United States continues to decline as a result of economic, market and regulatory factors. Consolidation has not, however, resulted in a material reduction of the number of customers or financial accounts serviced by the financial industry as a whole. Our focus on long-term client relationships and recurring, transaction-oriented products and services has reduced the impact that consolidation has on us. In addition, our revenue is diversified. Our top client represents approximately 5% of our annual revenue, and the next 49 financial institution clients represent approximately 17% of our annual revenue. The remaining 78% of our revenue is spread across the balance of our client base. Finally, we have clients that span the entire range of financial institutions in terms of asset size and we typically enter into multi-year agreements.

In 2009, due in part to the current state of the economy, we anticipate less account processing system switching by all depository institutions, which should benefit us given the number of account processing clients that we have. We also anticipate that demand will continue for products focused on gathering deposits, managing efficiency, and meeting risk and regulatory needs, all of which should translate to revenue opportunities for us. As a result, we believe that our sizable and diverse client base combined with our position as a leading provider of non-discretionary, recurring revenue-based products and services gives us a solid foundation that will continue to show strength, even in these difficult times. Our ongoing operations are reported in the Financial Institution Services (“Financial”) and Payments and Industry Products (“Payments”) business segments.

Financial

The businesses in our Financial segment provide financial institutions with the products and services they need to run their banking operations. Many financial institutions that previously developed their own software systems and maintained their own data processing operations have outsourced their data processing requirements by licensing software from third-parties or by contracting with third-party processors. This has allowed them to reduce costs and enhance their products and services. Outsourcing can involve the licensing of software, which eliminates the costly technical expertise within a financial institution, or the utilization of service bureaus, facilities management or resource management capabilities. Within the Financial segment, we provide banks, thrifts and credit unions with account processing services, item processing services, loan origination and servicing products, cash management and consulting services, and other products and services that support numerous types of financial transactions.

Payments

The businesses in our Payments segment provide products and services that address a range of technology needs for the financial services industry, including: Internet banking, electronic bill payment, electronic funds transfer and debit processing, fraud and risk management capabilities, card and print personalization services, check imaging and investment account processing services for separately managed accounts. We believe that the

2

integration of our Internet banking and electronic bill payment and settlement capabilities with our account processing and risk management solutions creates a compelling value proposition for clients.

Corporate Transactions in 2008

In January 2008, we completed the sale of a majority of our health businesses (“Fiserv Health”) to UnitedHealthcare Services, Inc. for approximately $480 million, net of income taxes and transaction costs. In February 2008, we completed the first of two transactions to dispose of our Investment Support Services segment (“Fiserv ISS”) by selling Fiserv Trust Company and the accounts of our institutional retirement plan and advisor services operations to TD AMERITRADE Online Holdings, Inc. for approximately $200 million, net of income taxes and transaction costs. In a second transaction, Robert Beriault Holdings, Inc. has agreed to acquire the remaining accounts and net capital of Fiserv ISS, including the investment administration services business which provides back office and custody services for individual retirement accounts. This portion of the Fiserv ISS disposition remains subject to customary closing conditions and regulatory approval by the Federal Deposit Insurance Corporation (the “FDIC”). We also completed the sale of three other subsidiaries in 2008, Del Mar Database, Inc., Insurance Wholesalers Insurance Services, Inc., and CareGain, Inc. The financial results of these businesses are reported as discontinued operations for all periods presented.

In July 2008, we completed the sale of a 51% interest in substantially all of the businesses in our Insurance segment (“Fiserv Insurance”) to Trident IV, LP. We received cash proceeds of approximately $500 million and a $30 million note. Beginning on July 15, 2008, we no longer consolidate revenues and expenses of Fiserv Insurance and report our 49% share of net income as a separate line item on our statement of income.

In 2008, we acquired: i_Tech Corporation, a provider of outsourced account and payment processing services; The Data Center, a data center and reseller of the Fiserv ITI Premier banking system; and the CashMaster cash forecasting product.

Our Strategy

Our vision is to be a global leader in transaction-based technology solutions. Our mission is to provide integrated technology and services solutions which enable best-in-class results for our clients. To meet these goals, we are implementing a series of strategic initiatives that we refer to as “Fiserv 2.0.” We are focused on operating businesses where we have: deep industry expertise that enables us to serve the market with high effectiveness; a strong competitive position, currently or via a clear path in the foreseeable future; long-term, trusted, ongoing client relationships which are not based on one-time transactions; differentiated solutions that deliver higher-than-normal value to our clients through integration and innovation; and strong management to execute strategies in a disciplined manner. Consistent with this focus, we are implementing the following strategic platforms:

Enhanced Client Relationship Value. We plan to increase the number and breadth of our client relationships by, among other matters, implementing tighter integration across our product and services groups, bundling more products and services to deliver improved value propositions, and streamlining our service and support processes.

Acquisitions. We expect to acquire businesses when we identify: a compelling strategic need, such as a product, service or technology that helps fill a specific market requirement; an opportunity to change market dynamics; a way to achieve business scale; or some similar consideration.

Innovation. We seek to be an innovation leader in all of our key markets, leveraging our assets and capabilities to be at the forefront of our markets. We expect to explore these opportunities both domestically and abroad.

Operational Excellence. We believe we can improve our performance by using the opportunities created by our size and scale. For example, we expect to improve our performance by more effectively using our consolidated buying power and shared utility structures to provide savings.

3

Greater Capital Discipline. Finally, we intend to make capital allocation decisions based on the investments that offer the best prospects for our long-term growth and profitability. These investments may include, among other matters, internal investment, repurchases of our own shares or debt, capital improvements or acquisitions.

We intend to continue to integrate our leading Internet banking, electronic billing and payment, and software technologies with our account processing offerings to make it easier for our clients to take advantage of ever-changing market opportunities and to deliver new or enhanced services to their customers.

Principal Solutions and Services

Financial information regarding our business segments is included in Note 9 to the consolidated financial statements on page 54.

Financial

We provide products and services to meet the financial technology needs of banks, credit unions, thrift and savings institutions, and leasing and finance companies. Many of the products and services that we provide are sold as an integrated solution to our clients and include account, lending, item and payments processing.

Account Processing

We provide integrated account servicing and management information functions for our bank, thrift and credit union clients, as well as ancillary value-added products and services that complement the account processing solutions. Account processing solutions include systems that process customer deposit and loan accounts, an institution’s general ledgers, central information files and other financial information. These solutions also include extensive security, report generation and other features that financial institutions need to process transactions for their depositors and other customers, as well as to meet their regulatory compliance requirements and their own management information needs. Account processing solutions are offered through online data transmission connections to our data processing centers, often called “service bureaus,” or as stand-alone, in-house licensed software for installation on client-owned computer systems. Third party data processing centers also license our software for use in providing services to their clients.

While many of our clients contract to obtain all or a majority of their data processing requirements from us, the modular design of many of our service bureau and software solutions allows clients to start with one application, such as a deposit system, and, as needed, add applications and features developed by us or by third parties. We support a broad range of terminals and other client-owned peripheral devices manufactured by a variety of vendors. This support capability reduces our clients’ initial conversion expenses, enhances existing clients’ ability to change equipment and broadens our market.

| • | Bank and Thrift Account Processing Solutions. The principal service bureau solutions used by banks, thrifts and savings institutions are: Premier, Cleartouch, Precision, Base, Signature and Source One. We also offer in-house licensed software solutions to our banking clients, including Premier, Precision and Signature. The Signature system is available both domestically and internationally. |

| • | Credit Union Account Processing Solutions. The principal account processing solutions primarily used by credit unions are: Advantage, Charlotte, CUBE, CubicsPlus, CUSA, DataSafe, OnCU, Galaxy, Premier, Reliance, Spectrum, and XP2. These solutions are offered in a service bureau environment, as an in-house licensed software system or in both delivery modes. |

Lending and Item Processing Solutions

We offer lending and item processing solutions to financial institutions and other financial intermediaries. We provide item processing and imaging systems via in-house solutions or in a service bureau environment to account processing clients as well as to those who do not utilize our account processing systems. Our item

4

processing services include source capture solutions via a web-based platform for check image capture at branch, merchant, consumer, ATM and regional centers. Through the Fiserv Clearing Network, we provide complete check clearing and image exchange services. We provide image archive services with online retrieval and full disaster backup, and a number of check imaging products that enable banks to leverage the processes provided for in the Check Clearing Act of the 21st Century. Our ACH software, PEP+®, enables payments to be originated and received through the ACH system, and, together with our PEP+reACHTM product, allows returned checks, checks at the point-of-sale, and checks sent to a lockbox to be converted to electronic payments. Our account reconciliation software, ARP/SMSTM, is an online, real-time positive pay and reconcilement system that enables customers to monitor deposits and identify duplicate items, which reduces their exposure to check fraud and helps them manage electronic check conversion. Our compliance solutions enable financial institutions, corporations and government agencies to maintain compliance with state and federal regulations applicable to them. We also provide consulting services, business operations services and software products that facilitate the transformation of our clients’ payments environment. We enhance a client’s ability to achieve its goals by enabling it to identify, select and implement the most effective and cost-efficient strategies. Finally, we offer traditional item processing services, including image capture, proof of deposit, in-clearings, statements, exception and return processing and fraud detection.

Our lending businesses offer a variety of products and services, including: valuation services, portfolio analytical services and real estate settlement services; automotive loan origination systems, lease and loan servicing products, default mitigation and business process outsourcing services; and a mortgage loan servicing platform and loan origination and tracking systems.

We also provide software, maintenance, support and consulting services primarily to large global financial service providers and other companies to support their ACH, account reconciliation, compliance, check and remittance payment processing, fraud and risk management and cash logistics needs. These products are designed to improve operational efficiency and contribute to increased profitability. We generally grant non-exclusive, non-transferable licenses to use our application software.

Payments

E-Banking

Our e-banking business is comprised of our online bill payment products and our online banking and cash management products. Financial institutions can offer our bill payment services to consumers either through a hosted application, known as CheckFree RXP, or through various protocols that link online banking applications to our Genesis billing and payment system. CheckFree RXP allows our clients’ customers to: manage household bills via an easy-to-use, online tool; view relevant billing and payment information; pay and manage all of their bills at one location; experience the same speed of payment they would normally have at a biller’s site; and conveniently make next-day payments to many of the companies with which they do business.

We use our Genesis platform to process the vast majority of the payment transactions that we process, which enables us to improve our economies of scale. Once a consumer has accessed the system through a financial institution, he or she can elect to pay an electronic bill delivered by us or can instruct the system to pay any individual or company within the United States. We complete this payment request either electronically, using the Federal Reserve’s ACH network or other electronic methods such as MasterCard RPPS service or Visa ePay, or by issuing a paper check or draft. In 2008, we processed more than 1.3 billion online bill payment transactions. We also provide the Paytraxx™ bill payment solution which delivers a broad range of functionality and features for both consumer and business bill payment.

Our principal online consumer and business banking product is VoyagerTM, a software platform upon which we have built a number of software applications to support multiple lines of banking businesses. Using universal standards, it has been designed to be highly scalable to meet the evolving needs of our clients. This structure enables our clients to deploy new Internet-based financial services by adding applications to our platform at any

5

time and by integrating future applications to any Internet connected point-of-presence. We also provide a series of treasury management solutions, including online business banking, commercial cash management, remote deposit, and corporate data exchange, under our BANKLINK® brand.

Mobile Money is a new product that seeks to capitalize on the growth of the mobile channel as an access and delivery point for banking and payment services. Mobile Money provides a variety of mobile banking and payments services, including balance inquiry, transaction history, bill payment and transfers, through a mobile device to our financial institution clients and their customers. It enables financial institutions to reach more consumers via the mobile channel than any other single technology solution because it supports all three mobile access modes: browser, SMS or text banking, and mobile application. Mobile Money can also be integrated into our account processing, online banking and bill payment products.

Biller Business

We believe that consumers will continue to shift their financial transactions from traditional paper-based methods to electronic methods if they have easy-to-access, easy-to-use, secure and cost-effective methods of receiving and paying their bills electronically. In 2008, through our electronic biller services business, we delivered approximately 300 million electronic bills to consumers through our various distribution channels. Consumers access our electronic billing and payment solutions via numerous hosted channels, including through a financial institution’s Internet portal, through the billers’ Internet sites, and through our biller services internet portal, www.mycheckfree.com. Additionally, consumers can make their bill payments, including emergency or expedited payments, through our agent-assisted, Internet or interactive voice response phone tools and our nationwide walk-in bill payment locations. These diverse services allow the customers of our clients to pay their bills wherever and however they feel most comfortable. Our electronic biller services business also offers a host of club management and electronic financial transaction services within the health and fitness industry.

Risk Management

Our risk management business provides a suite of products and services, including financial crime, compliance, anti-money laundering, fraud prevention, market surveillance and employee fraud detection solutions. Our offerings in this market include Fiserv KRM, Fraud Manager, Fraud Detection System, Fraudlink and Fraudguard.

Credit Processing

Our feature-rich credit products and services fulfill a wide range of bank card, retail, commercial and consumer credit processing requirements through an integrated, full-service credit management solution that utilizes a globally recognized processing platform. Our credit processing system is a real-time product that is scalable to multi-million account portfolios. It provides credit decisioning, authorization processing, online cardholder account management, customer service case management, letters, card production, statements, targeted marketing programs, collections, and recovery management. Our end-to-end solution offers efficient and cost-effective processing solutions to all types of credit issuers.

EFT

Fiserv EFT, a leader in the electronic funds transfer marketplace, provides a total payments solution through a variety of products, services and strategies. We offer ATM, credit and point of sale PIN-based debit transaction processing, Visa and MasterCard signature debit processing, ATM driving and monitoring, electronic benefits transfer switching and national and regional network access. We own the ACCEL/Exchange Network and operate approximately 20,000 ATMs. Fiserv EFT has a highly recurring revenue model with an average contract term of more than five years. Comprehensive integration with our account processing products and services allows us to drive down costs and leverage efficiencies for our clients through enterprise offerings in areas such as risk management and loyalty rewards. Fiserv EFT generates over 85% of its revenues from transactions performed by customers and members of our financial institution clients. Fiserv EFT’s clients include more than

6

2,800 banks and credit unions of all asset sizes, resellers (via both business alliance and remarketer agreements), independent sales organizations and merchant acquirers across the United States. In 2008, we processed approximately six billion ATM and debit transactions, making us one of the largest financial transaction processors in the nation.

Output Solutions

Our output solutions business provides clients with: electronic document management through our Electronic Document Delivery products and services; card manufacturing, personalization and mailing, statement production and mailing, and design and fulfillment direct mail solutions; and forms distribution, laser printing and mailing, and office supplies.

Investment Services

We provide a range of technology platforms to help approximately 350 financial institutions, including broker dealers, global asset managers, investment advisors, banks and insurance companies, deliver portfolio management, enhanced trading solutions, performance measurement, reporting services, corporate actions, billing, and trading automation to their clients. Our fee-based investment management clients are typically sponsors or managers in the managed accounts and wealth management market that offer separately managed accounts, unified managed accounts, mutual fund advisory accounts, and investment management products, or global institutional money managers, managing investments of institutions and high net worth individuals. Our primary product is a real-time portfolio management and trading system used by nine of the top ten largest brokerage firms, based on assets under management, and eight of the top ten largest asset managers offering managed accounts.

Servicing the Market

Our mission is to provide integrated technology and services solutions that enable best-in-class results for our clients. This principle is backed by our dedication to providing excellent client service and support no matter the size of the client. The markets for our account and transaction processing services have specific needs and requirements, with strong emphasis placed by clients on flexibility, quality, comprehensiveness and integration of product lines, service reliability, timely introduction of new products and features, cost effectiveness, and service excellence. Through our multiple product and service offerings, we service the needs of our clients which range in size from start-ups to the largest financial services providers.

We offer clients a selection of information management and data processing services designed to meet the specific needs of the ever-changing financial services industry. We believe that our financial strength and primary focus on the financial services industry enhances our ability to develop and support products and services and service our clients. In addition, we believe that our commitment of substantial resources to training and technical support helps us to retain clients. We conduct the majority of our new and ongoing client training in our technology centers, where we maintain fully equipped demonstration and training facilities that contain equipment used in the delivery of our services. We also provide on-site training services and online education to clients.

Product Development

To meet the changing technology needs of our clients, we continually develop, maintain and enhance our products and systems. In 2008, 2007 and 2006, product development expenses represented approximately 8%, 7% and 7%, respectively, of our total revenues. Our network of development and financial information technology centers apply the expertise of multiple teams to design, develop and maintain specialized processing systems around our multiple technology platforms. The applications of our account processing systems meet the preferences and diverse requirements of the international, national, regional or local market-specific financial service environments of our clients. In developing our products, we stress interaction with and responsiveness to the needs of our clients, including customization of software to meet client needs. We have adopted web services

7

and service-oriented architecture principles in our software development practices so that we and our clients can benefit from the efficient development of technology. We have implemented a nationwide networking infrastructure among billers, consumers, retail agents and financial institutions to transfer transaction data among them and to complete electronic billing and payment transactions. We provide dedicated solutions that are designed, developed, maintained and enhanced according to each client’s goals for service quality, business development, asset and liability mix, and local market positioning as well as other user-defined parameters.

Intellectual Property

We regard our transaction processing services and related products and our software as proprietary, and utilize a combination of patent, copyright, trademark and trade secrecy laws, internal security practices and employee and third party non-disclosure agreements for protection. We believe that legal protection of our software, while important, is less significant than the knowledge and experience of our management and personnel and their ability to develop, enhance and market new products and services. The majority of our patents cover various electronic billing and payment innovations, other financial software products or services, or aspects of our separately managed accounts services. We believe that we possess all proprietary rights necessary to conduct our business.

Competition

Financial

The market for information technology products and services within the financial industry is highly competitive. Our principal competitors include internal data processing departments, data processing affiliates of large companies and large computer hardware manufacturers, independent computer service firms and processing centers owned and operated as user cooperatives. Some of these competitors possess substantially greater financial, sales and marketing resources than we do. Competition for in-house data processing and software departments is intensified by the efforts of computer hardware vendors which encourage the growth of internal data centers and consulting service providers who assist these departments with the design and implementation of customized software solutions. Our software products compete in several different market segments and geographies, including with large diversified computer software and service companies and independent suppliers of software products.

Competitive factors for account processing services include product quality, service reliability, product line comprehensiveness and integration, timely introduction of new products and features, and price. We believe that we compete favorably in each of these categories. In addition, we believe that our position as an independent vendor, rather than as a cooperative, an affiliate of a larger corporation or a hardware vendor, is a competitive advantage. We compete with vendors that offer similar transaction processing products and services to financial institutions, including Fidelity National Information Services, Inc., Metavante Technologies, Inc., Jack Henry and Associates, Inc., and Open Solutions, Inc. There has been significant consolidation among providers of information technology products and services to financial institutions, and we believe this consolidation will continue in the future.

Payments

Our primary competition in the electronic commerce market is the traditional paper-based method of receiving and paying bills. In addition, the possibility of billers and financial institutions continuing to use or deciding to create in-house systems to handle their own electronic billing and payment transactions, and their own Internet banking solutions in the case of financial institutions, remains a significant competitive threat. In-house solutions have been, and will continue to be, an option for our clients and a competitive factor facing our business.

Metavante Technologies, Inc. and Online Resources Corporation compete with us most directly as full service banking, billing and bill payment competitors. A number of other companies compete with us by providing some, but not all, of the services that make up our complete e-bill and electronic pay anyone service, including Yodlee, MasterCard International and Visa. In the area of Internet consumer banking, we primarily

8

compete with other companies that provide outsourced Internet finance solutions to large financial institutions, including S1 Corporation, and with companies that offer software platforms designed for internal development of Internet-based financial services software. We expect competition to continue to increase as new companies enter our markets and existing competitors expand their product lines and services. In addition, many companies that provide outsourced Internet finance solutions are consolidating, creating larger competitors with greater resources and broader product lines. Our investment services business competes primarily with providers of portfolio accounting software and outsourced services and with in-house solutions developed by large financial institutions.

Government Regulation

Our data processing and electronic commerce subsidiaries are generally not directly subject to federal or state regulations specifically applicable to financial institutions such as banks, thrifts and credit unions. However, as a provider of services to these financial institutions, our data processing and electronic commerce operations are examined on a regular basis by the FDIC, the Federal Reserve Bank, the National Credit Union Association, the Office of Thrift Supervision, the Office of the Comptroller of the Currency and various state regulatory authorities. Because we use the Federal Reserve’s ACH network to process many of our transactions, we are subject to the Federal Reserve Board’s rules with respect to its ACH network. In addition, independent auditors annually review many of our operations to provide internal control evaluations for our clients’ auditors and regulators.

In conducting our electronic commerce business, we are subject to various laws and regulations relating to the electronic movement of money. In 2001, the USA Patriot Act amended the Bank Secrecy Act (“BSA”) to expand the definition of money services businesses so that it may include businesses such as CheckFree. CheckFree submitted a request for an administrative ruling from the Financial Crimes Enforcement Network (“FinCEN”) in 2002 with respect to whether FinCEN views CheckFree as a money services business. To date, CheckFree has not received a ruling from FinCEN. If CheckFree’s business is determined to be a money services business, then CheckFree will have to register with FinCEN as a money services business and be regulated as such. Also, nearly all states and the District of Columbia have enacted statutes that require entities engaged in money transmission, the sale of traveler’s checks (including money orders) and the sale of stored value cards to register as a money transmitter with that jurisdiction’s banking department, and CheckFree has registered as a money transmitter where required. In addition, our electronic commerce business is subject to the regulations of the Office of Foreign Assets Control, the electronic funds transfer rules embodied in Regulation E promulgated by the Federal Reserve Board and, when conducting certain transactions, the Gramm-Leach-Bliley Act.

Our walk-in bill payment service is registered as a money service business with FinCEN. We have established and maintain a program to provide a system of controls and procedures that we believe is reasonably designed to detect, prevent and report actual or suspected violations of the BSA, money laundering statutes, anti-terrorism statutes and other illicit activity. We requested an administrative ruling from FinCEN in 2003 regarding whether FinCEN considers all or some of our walk-in bill payment service to be a money services business. We made a supplemental ruling request in 2008. FinCEN has not yet issued a ruling. If our walk-in bill payment business is determined to be a money services business, then we will be regulated accordingly. If not, we will deregister the walk-in bill payment service as a money service business. In addition, we currently maintain 44 licenses to comply with the various money transmitter statutes mentioned above, and we are subject to annual audits by such jurisdictions.

From time to time, in order to comply with our obligations under federal and state laws, we may be required to comply with annual reporting or licensing requirements or to implement operating policies and procedures to protect, among other matters, the privacy and security of our clients’ information.

9

Employees

We have approximately 20,000 employees, many of whom are specialists in our information management centers and related product and service businesses. This service support network includes employees with backgrounds in computer science and the financial and insurance industries, often complemented by management and other employees with direct experience in banks, thrifts, credit unions, savings institutions, and other financial services environments. Our employees provide expertise in: programming, software development, modification and maintenance; computer operations, network control and technical support; client services and training; business process outsourcing; item and mortgage processing; system conversions; sales and marketing; and account management.

None of our employees in the United States are represented by a union and there have been no work stoppages, strikes or, to our knowledge, attempts to organize. The service nature of our business makes our employees an important corporate asset. Although the market for qualified personnel is competitive, we have not experienced significant difficulty with hiring or retaining our staff of top industry professionals. In assessing potential acquisition candidates, the quality and stability of the prospective company’s staff are emphasized.

Available Information

Our website address is www.fiserv.com. We are not including the information provided on our website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K. We make available free of charge (other than an investor’s own Internet access charges) through our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the Securities and Exchange Commission.

You should carefully consider each of the risks described below, together with all of the other information contained in this Annual Report on Form 10-K, before making an investment decision with respect to our securities. If any of the following risks develop into actual events, our business, financial condition or results from operations could be materially and adversely affected and you may lose all or part of your investment.

Our business may be adversely impacted by U.S. and global market and economic conditions.

For the foreseeable future, we expect to continue to derive most of our revenue from products and services we provide to the financial services industry. Given this concentration, we may be particularly exposed to the current global economic recession. For example, our Financial segment has been negatively impacted by a significant reduction in home-equity processing revenues resulting from the decline in the U.S. mortgage markets. A poor economic environment could result in significant decreases in demand by current and potential clients for our products and services, which could have a material adverse effect on our business, results of operations and financial condition.

Consolidations and failures in the banking and financial services industry could adversely affect our revenues by eliminating existing or potential clients and making us more dependent on a more limited number of clients.

Many banks and financial institutions are experiencing significant operating losses, including many of our clients. In some cases, these operating losses have resulted in the failure and/or consolidation of banks and other financial institutions. Failures, mergers and consolidations of banks and financial institutions reduce the number of our clients and potential clients, which could adversely affect our revenues. Further, if our clients fail or merge with, or are acquired by, other entities that are not our clients, or that use fewer of our services, they may discontinue or reduce their use of our services. It is also possible that the larger banks or financial institutions

10

resulting from mergers or consolidations would have greater leverage in negotiating terms with us or could decide to perform in-house some or all of the services which we currently provide or could provide. Any of these developments could have a material adverse effect on our business, results of operations and financial condition.

We operate in a competitive business environment, and if we are unable to compete effectively, our results of operations and financial condition may be adversely affected.

The market for our services is competitive. Our competitors vary in size and in the scope and breadth of the services they offer. Some of our competitors have substantial resources. Since many of our larger potential clients have historically developed their key applications in-house, we often compete against our potential clients’ in-house capabilities. Our existing large clients may also explore the possibility of internally performing portions of the outsourced Internet banking and electronic billing and payment services that we provide to them. In addition, we expect that the markets in which we compete will continue to attract new competitors and new technologies, including international providers of similar products and services to ours, having a lower cost structure. We cannot provide any assurance that we will be able to compete successfully against current or future competitors or that competitive pressures faced by us in the markets in which we operate will not materially and adversely affect our business, financial condition and results of operations.

If we fail to adapt our products and services to changes in technology or in the marketplace, or if our ongoing efforts to upgrade our technology are not successful, we could lose clients.

The markets for our products and services are characterized by constant technological changes, frequent introductions of new products and services and evolving industry standards. Our ability to enhance our current products and services and to develop and introduce innovative products and services that address the increasingly sophisticated needs of our clients and their customers will significantly affect our future success. We may not be successful in developing, marketing or selling new products and services that meet these changing demands. In addition, we may experience difficulties that could delay or prevent the successful development, introduction or marketing of these services, or our new services and their enhancements may not adequately meet the demands of the marketplace or achieve market acceptance. We continually engage in significant efforts to upgrade our products and services. If we are unsuccessful in completing or gaining market acceptance of new technology, it would likely have a material adverse effect on our ability to retain existing clients or attract new ones.

If we are unable to renew client contracts at favorable terms, we could lose clients and our results of operations and financial condition may be adversely affected.

Failure to achieve favorable renewals of client contracts could negatively impact our business. Our contracts with our clients for account processing services generally run for a period of three to five years in our Financial segment and provide for termination fees upon early termination. Our contracts with financial services organizations for electronic commerce services generally provide for terms of two to five years. At the end of the contract term, clients have the opportunity to renegotiate their contracts with us and to consider whether to engage one of our competitors to provide products and services. In addition, it is possible that one or more clients could seek to renegotiate terms with us. If we are not successful in achieving high renewal rates and favorable contract terms, our results of operations and financial condition may be adversely affected.

The market for our electronic transaction services is evolving and may not continue to develop or grow rapidly enough to sustain profitability.

If the number of electronic transactions does not continue to grow or if consumers or businesses do not continue to adopt our services, it could have a material adverse effect on our business, financial condition and results of operations. We believe future growth in the electronic transactions market will be driven by the cost, ease-of-use, and quality of products and services offered to consumers and businesses. In order to consistently increase and maintain our profitability, consumers and businesses must continue to adopt our services. In addition, if we are unable to continue to decrease the cost of processing transactions, our margins could decrease, which could have a material adverse effect on our business, financial condition and results of operations. Our

11

electronic commerce business also relies on contracts with financial services organizations, businesses, billers, Internet portals and other third parties to provide branding for our electronic commerce services and to market our services to their customers. These contracts are an important source of the growth in demand for our electronic commerce products. If any of these third parties abandons, curtails or insufficiently increases its marketing efforts, it could have a material adverse effect on our business, financial condition and results of operations.

Our balance sheet includes significant amounts of goodwill and intangible assets. The impairment of a significant portion of these assets would negatively affect our financial results.

Our balance sheet includes goodwill and intangible assets that represent approximately 70% of our total assets at December 31, 2008. These assets consist primarily of goodwill and identified intangible assets associated with our acquisitions, including significant goodwill and intangible assets associated with our acquisition of CheckFree. On at least an annual basis, we assess whether there have been impairments in the carrying value of goodwill and intangible assets. If the carrying value of the asset is determined to be impaired, then it is written down to fair value by a charge to operating earnings. An impairment of a significant portion of goodwill or intangible assets could materially negatively affect our results of operations.

We may be obligated to indemnify the purchasers of Fiserv Health, Fiserv ISS or Fiserv Insurance pursuant to the terms of the relevant purchase and sale agreements.

In 2008, we completed the sale of several significant businesses. In connection with the sales, we made representations and warranties about the businesses and their financial affairs and agreed to be liable for certain liabilities resulting from our operation of such businesses prior to the sale. Pursuant to the terms of the agreements, we may be obligated to indemnify the purchasers for certain material adverse events arising out of or related to our prior operation of the business and for any breach of a representation or warranty. Our obligation to indemnify a purchaser in the future could have a material adverse effect on our business, results of operations and financial condition.

We may not complete the sale of the remainder of Fiserv ISS in the time frame we anticipate, or at all, and we are subject to the risks of the operation of that business.

We have entered into an agreement to sell the remainder of Fiserv ISS, which primarily provides back office and custody services for self-directed individual retirement accounts. The completion of the sale is subject to a number of risks and uncertainties, including: the satisfaction of the conditions to the completion of the sale; the parties to the sale obtaining all necessary regulatory approvals, including approval from the FDIC; legal proceedings that may be instituted against us or others; the occurrence of any event, change or other circumstance that could give rise to the termination of the applicable disposition agreement; and our ability to obtain the expected proceeds from the disposition. These and other factors could cause our ability to complete the disposition on the terms and within the time frame anticipated to be different than expected. Therefore, there is no guarantee that we will be able to complete the transaction. We are subject to the risks of operating the remainder of the Fiserv ISS business until we complete the sale, or if we are unable to complete the sale, which include compliance with applicable regulations, data security risks, and potential legal proceedings with respect to the operation of this business. Such risks could have a material adverse effect on our business, financial condition and results of operations.

We may be sued for infringing on the intellectual property rights of others.

Third parties may claim that we are infringing on their intellectual property rights. We may violate the rights of others without our knowledge. We may expose ourselves to additional liability if we agree to indemnify our clients against third party infringement claims. If a litigant establishes that we are infringing its intellectual property rights, or that our intellectual property rights are invalid, we may be forced to change our products, services, or manufacturing processes, and such changes may be expensive or impractical. We may then be forced to seek royalty or license agreements from such litigant. If we are unable to agree on acceptable terms, we may

12

be required to discontinue the sale of key products or halt other aspects of our operations. In addition, we may also be liable for significant financial damages for a violation of intellectual property rights, and we may incur significant expense in connection with indemnifying our clients against losses suffered by them. Any adverse result related to violation of third party intellectual property rights could materially and adversely harm our business, financial condition and results of operations. Even if intellectual property claims brought against us are without merit, they may result in costly and time consuming litigation, and may divert our management and key personnel from operating our business.

Security breaches or computer viruses could harm our business by disrupting our delivery of services and damaging our reputation.

We electronically receive, process, store and transmit our clients’ and their customers’ sensitive information. Unauthorized access to our computer systems could result in the theft or publication of confidential information or the deletion or modification of records or could otherwise cause interruptions in our operations. These concerns about security are increased when we transmit information over the Internet. Computer viruses can be distributed and rapidly spread over the Internet. Computer viruses could infiltrate our systems, disrupting our delivery of services and making our applications unavailable. Any inability to prevent security breaches or computer viruses could have a negative impact on our reputation, could expose us to liability, could decrease market acceptance of electronic transactions and could cause our present and potential clients to choose another service provider. Any of these developments could have a material adverse effect on our business, results of operations and financial condition.

Increased leverage may harm our financial condition and results of operations.

As of December 31, 2008, we had approximately $4.1 billion of total long-term debt, including current maturities. We and our subsidiaries may incur additional indebtedness in the future. Our current level of indebtedness and any future increase in our level of indebtedness could: increase our cash requirements to support the payment of interest; increase our vulnerability to adverse changes in general economic and industry conditions; decrease our ability to obtain additional financing for working capital, capital expenditures, general corporate or other purposes; limit our flexibility in planning for, or reacting to, changes in our business and our industry; and limit our flexibility to make acquisitions. Our ability to make payments of principal and interest on our indebtedness depends upon our future performance, which will be subject to general economic conditions and financial, business and other factors affecting our consolidated operations, many of which are beyond our control. If we are unable to generate sufficient cash flow from operations in the future to service our debt and meet our other cash requirements, we may be required, among other things: to seek additional financing in the debt or equity markets; to refinance or restructure all or a portion of our indebtedness; or to reduce or delay planned capital or operating expenditures. Such measures might not be sufficient to enable us to service our debt and meet our other cash requirements. In addition, any such financing, refinancing or sale of assets might not be available at all or on economically favorable terms, particularly given current economic and credit market conditions.

We may not realize the expected benefits of the acquisition of CheckFree.

Our ability to realize the anticipated benefits of the acquisition will depend, in part, on our ability to successfully integrate the businesses of Fiserv and CheckFree, and we cannot assure you that the combination of the two companies will result in the realization of the anticipated economic, operational and other benefits from the acquisition within expected time frames or at all. In particular, we have estimated that we will be able to achieve annual cost savings of more than $100 million and annual revenue synergies of more than $125 million over the next several years as we integrate the CheckFree acquisition. Our ability to achieve those savings and synergies depends on a number of factors, some of which are beyond our control, and we will not be able to fully assess these opportunities until after the integration is complete. As a result, the integration of CheckFree may not generate expected revenue synergies, cross-selling opportunities or cost savings on the expected time frames or at all. If we are unable to successfully implement our planned integration with CheckFree and realize the expected benefits from the acquisition, our results of operations and cash flows could be adversely affected.

13

Our acquisition strategy subjects us to risks, including increased debt, assumption of unforeseen liabilities and difficulties in integrating operations.

A major contributor to our growth in revenues and earnings since our inception has been our ability to identify, acquire and integrate complementary businesses. We anticipate that we will continue to seek to acquire complementary businesses, products and services. We may not be able to identify suitable acquisition candidates in the future, which could adversely affect our future growth. Businesses we acquire may not perform as well as expected or be more difficult to integrate and manage than expected, which could adversely affect our business and financial results. We may not be able to fully integrate all aspects of acquired businesses successfully or fully realize the potential benefits of bringing them together. In addition, the process of integrating these acquisitions may disrupt our business and divert our resources.

These risks may arise for a number of reasons: we may not be able to find suitable businesses to acquire at affordable valuations or on other acceptable terms; we face competition for acquisitions from other potential acquirers; we may need to borrow more money from lenders or sell equity or debt securities to the public to finance future acquisitions and the terms of these financings may be adverse to us; changes in accounting, tax, securities or other regulations could increase the difficulty or cost for us to complete acquisitions; we may incur unforeseen obligations or liabilities in connection with acquisitions; we may need to devote unanticipated financial and management resources to an acquired business; we may not realize expected operating efficiencies or product integration benefits from an acquisition; we could enter markets where we have minimal prior experience; and we may experience decreases in earnings as a result of non-cash impairment charges.

Operational failures in our outsourcing or transaction processing facilities could harm our business and reputation.

An operational failure in our outsourcing or transaction processing facilities could cause us to lose clients. Damage or destruction that interrupts our provision of services could damage our relationship with clients and may cause us to incur substantial additional expense to repair or replace damaged equipment. In addition, we may also be liable to third parties or owe service credits to our clients. A prolonged interruption of our services or network that extends for more than several hours could cause us to experience data loss or a reduction in revenues as a result of such interruption. In addition, a significant interruption of service could have a negative impact on our reputation and could cause our present and potential clients to choose another service provider.

We may experience software defects, development delays or installation difficulties, which would harm our business and reputation and expose us to potential liability.

Our services are based on sophisticated software and computing systems, and we may encounter delays when developing new applications and services. Further, the software underlying our services has occasionally contained and may in the future contain undetected errors or defects when first introduced or when new versions are released. In addition, we may experience difficulties in installing or integrating our technologies on platforms used by our clients. Defects in our software, errors or delays in the processing of electronic transactions or other difficulties could result in interruption of business operations, delay in market acceptance, additional development and remediation costs, diversion of technical and other resources, loss of clients, negative publicity or exposure to liability claims. Although we attempt to limit our potential liability through disclaimers and limitation of liability provisions in our license and client agreements, we cannot be certain that these measures will successfully limit our liability.

Misappropriation of our intellectual property and proprietary rights could impair our competitive position.

Our ability to compete depends upon proprietary systems and technology. We actively seek to protect our proprietary rights. Nevertheless, unauthorized parties may attempt to copy aspects of our services or to obtain and use information that we regard as proprietary. The steps we have taken may not prevent misappropriation of technology. Agreements entered into for that purpose may not be enforceable or provide us with an adequate

14

remedy. Effective patent, trademark, service mark, copyright and trade secret protection may not be available in every country in which our applications and services are made available. Misappropriation of our intellectual property or potential litigation concerning such matters could have a material adverse effect on our results of operations or financial condition.

If we fail to comply with applicable regulations our businesses could be harmed.

Our financial services data processing subsidiaries are not directly subject to federal or state regulations specifically applicable to financial institutions such as banks, thrifts and credit unions. However, as a provider of services to these financial institutions, our data processing operations are examined on a regular basis by various federal and state regulatory authorities. If we fail to comply with any applicable regulations, we could be exposed to suits for breach of contract or to governmental proceedings, our client relationships and reputation could be harmed and we could be inhibited in our ability to obtain new clients. In addition, the future enactment of more restrictive laws or rules on the federal or state level, or, with respect to our international operations, in foreign jurisdictions on the national, provincial, state or other level, could have an adverse impact on our results of operations or financial condition.

Our failure to comply with a series of complex regulations in our walk-in payment business could subject us to liability.

CheckFreePay is licensed as a money transmitter in those states where such licensure is required. These licenses require us to demonstrate and maintain certain levels of net worth and liquidity and also require us to file periodic reports. In addition, this business is subject to regulation in the United States by FinCEN, including anti-money laundering regulations and certain restrictions on transactions to or from certain individuals or entities. The complexity of these regulations will continue to increase our cost of doing business. In addition, any violations of law may result in civil or criminal penalties against us and our officers or the prohibition against us providing money transmitter services in particular jurisdictions.

Item 1B. Unresolved Staff Comments

Not applicable.

We currently operate full-service data centers, software system development centers and item processing and back-office support centers in over 150 cities. We own 12 buildings and the remaining 195 locations where we operate our businesses are subject to leases expiring through 2009 and beyond. In addition, we maintain our own national data communication network consisting of communications processors and leased lines.

We believe our facilities and equipment are generally well maintained and are in good operating condition. We believe that the computer equipment that we own and our various facilities are adequate for our present and foreseeable business needs. We periodically upgrade our mainframe capability. We maintain our own, and contract with multiple service providers to provide, processing back-up in the event of a disaster. We also maintain copies of data and software used in our business in locations that are separate from our facilities.

In the normal course of business, we and our subsidiaries are named as defendants in lawsuits in which claims are asserted against us. Other than as described in Note 8 to the accompanying consolidated financial statements, in the opinion of management, the liabilities, if any, which may ultimately result from such lawsuits are not expected to have a material adverse effect on our consolidated financial statements.

Item 4. Submission of Matters to a Vote of Security Holders

During the fourth quarter of the fiscal year covered by this report, no matter was submitted to a vote of our security holders.

15

EXECUTIVE OFFICERS OF THE REGISTRANT

The names of our executive officers as of February 26, 2009, together with their ages, positions and business experience are described below:

| Name |

Age | Title | ||

| Jeffery W. Yabuki |

48 | President, Chief Executive Officer and Director | ||

| James W. Cox |

45 | Executive Vice President, Corporate Development | ||

| Thomas J. Hirsch |

45 | Executive Vice President, Chief Financial Officer, Treasurer and Assistant Secretary | ||

| Peter J. Kight |

52 | Vice Chairman and Director | ||

| Stephen E. Olsen |

48 | Executive Vice President and Group President, Depository Institution Services | ||

| Charles W. Sprague |

59 | Executive Vice President, General Counsel, Chief Administrative Officer and Secretary | ||

| Thomas W. Warsop III |

42 | Executive Vice President and Group President, Financial Institution Services | ||

Mr. Yabuki has been a director and our President and Chief Executive Officer since 2005. Before joining Fiserv, Mr. Yabuki served as Executive Vice President and Chief Operating Officer for H&R Block, Inc., a financial services firm, from 2002 to 2005. From 2001 to 2002, he served as Executive Vice President of H&R Block and from 1999 to 2001, he served as the President of H&R Block International. From 1987 to 1999, Mr. Yabuki held various executive positions with American Express Company, a financial services firm, including President and Chief Executive Officer of American Express Tax and Business Services, Inc.

Mr. Cox has served as Executive Vice President, Corporate Development since 2006. From 2003 to 2006, he served as President of our Health Solutions Group, and joined us in 2001 with the acquisition of Trewit, Inc., where he was President. Prior to that, Mr. Cox was a partner in Virchow Krause & Company, LLP, a public accounting and consulting firm.

Mr. Hirsch has served as Executive Vice President, Chief Financial Officer and Treasurer since 2006. Mr. Hirsch joined Fiserv in 1994 as a Divisional Assistant Controller, became Corporate Assistant Controller in 1996, Corporate Vice President in 1997, Corporate Controller in 1999 and Senior Vice President and Controller in 2002. Prior to joining us, Mr. Hirsch was an audit manager with Deloitte & Touche LLP.

Mr. Kight has been a director and Vice Chairman since 2007. Mr. Kight is the founder of CheckFree Corporation, which was acquired by Fiserv in 2007, and served as its Chairman and Chief Executive Officer since 1981. Mr. Kight is also director of Akamai Technologies, Inc., a publicly traded company that distributes computing solutions and services, and Manhattan Associates, Inc., a publicly traded company that provides supply chain planning and execution solutions.

Mr. Olsen joined Fiserv in 2007 in connection with our acquisition of CheckFree Corporation as Executive Vice President and President of our Internet Banking and Electronic Payments Group, and assumed his current position at the end of 2008. Prior to joining Fiserv, from 1997 to 2007, Mr. Olsen held a variety of positions at CheckFree, most recently as CheckFree’s Chief Operating Officer. From 1996 to 1997, Mr. Olsen served as Vice President, Chief Information Officer of Geac Computer Corporation. From 1990 to 1996, Mr. Olsen served as Vice President, Chief Information Officer of Dun & Bradstreet Software.

16

Mr. Sprague has served as Executive Vice President, General Counsel and Secretary since 1994 and as Chief Administrative Officer since 1999. He has been involved with our corporate and legal concerns since we were formed in 1984.

Mr. Warsop joined Fiserv in 2007 as Executive Vice President and President of our Financial Institutions Group and assumed his current position at the end of 2008. Prior to that, Mr. Warsop served for 17 years in various capacities, including Vice President, US Financial Services, at Electronic Data Systems Corp. (“EDS”), a publicly-traded global technology services company. He also served as a Vice President with EDS in the United Kingdom and as president of EDS’s Business Process Outsourcing unit in Asia Pacific.

17

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Price Information

Our common stock is traded on the Nasdaq Global Select Market under the symbol “FISV.” Set forth below is the high and low sales price of our common stock during the periods presented.

| 2008 | 2007 | |||||||||||

| Quarter Ended |

High | Low | High | Low | ||||||||

| March 31 |

$ | 56.80 | $ | 46.64 | $ | 55.08 | $ | 50.27 | ||||

| June 30 |

54.37 | 45.30 | 59.85 | 51.75 | ||||||||

| September 30 |

54.67 | 43.05 | 58.32 | 44.16 | ||||||||

| December 31 |

46.88 | 27.75 | 56.22 | 49.34 | ||||||||

At December 31, 2008, our common stock was held by 3,075 shareholders of record and by a significantly greater number of shareholders who hold shares in nominee or street name accounts with brokers. The closing sale price of our common stock on February 25, 2009 was $33.73 per share. We have never paid dividends on our common stock and we do not anticipate paying dividends in the foreseeable future. For additional information regarding our expected use of capital, refer to the discussion in this report under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

Issuer Purchases of Equity Securities

The table below sets forth information with respect to purchases made by or on behalf of us or any “affiliated purchaser” (as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934) of shares of our common stock during the three months ended December 31, 2008:

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(1) |

Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs(1) | |||||

| October 1 – 31, 2008 |

1,149,600 | $ | 36.92 | 1,149,600 | 5,679,700 | ||||

| November 1 – 30, 2008 |

3,416,461 | $ | 32.74 | 3,416,461 | 2,263,239 | ||||

| December 1 – 31, 2008 |

1,014,944 | $ | 32.23 | 1,014,944 | 1,248,295 | ||||

| Total |

5,581,005 | 5,581,005 | |||||||

| (1) | On July 2, 2008, we announced that our board of directors authorized the repurchase of up to 10 million shares of our common stock. This repurchase authorization does not expire. |

18

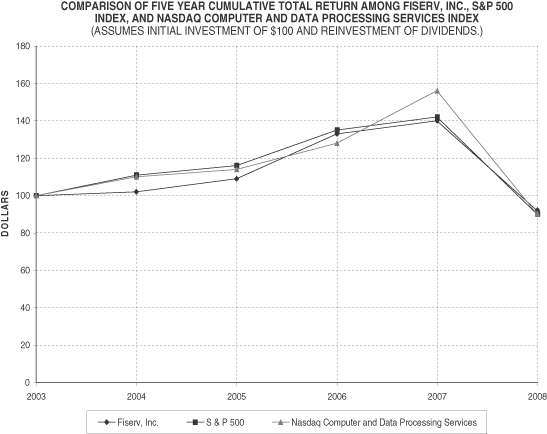

Stock Performance Graph

The stock performance graph and related information presented below is not deemed to be “soliciting material” or to be “filed” with the Securities and Exchange Commission or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filing.

The following graph compares the cumulative total shareholder return on our common stock for the five years ended December 31, 2008 with the S&P 500 Index and the NASDAQ Computer and Data Processing Services Index. The graph assumes that $100 was invested on December 31, 2003 in our common stock and each index and that all dividends were reinvested. No cash dividends have been declared on our common stock. The comparisons in the graph are required by the Securities and Exchange Commission and are not intended to forecast or be indicative of possible future performance of our common stock.

| December 31, | ||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | |||||||||||||

| Fiserv, Inc. |

$ | 100 | $ | 102 | $ | 109 | $ | 133 | $ | 140 | $ | 92 | ||||||

| S&P 500 |

100 | 111 | 116 | 135 | 142 | 90 | ||||||||||||

| Nasdaq Computer and Data Processing Services |

100 | 110 | 114 | 128 | 156 | 90 | ||||||||||||

19

Item 6. Selected Financial Data

The following data, which has been affected by acquisitions and dispositions, should be read in conjunction with the consolidated financial statements and related notes thereto included elsewhere in this Annual Report on Form 10-K.

| (In millions, except per share data) |

2008 | 2007 | 2006 | 2005 | 2004 | ||||||||||

| Total revenues |

$ | 4,739 | $ | 3,897 | $ | 3,544 | $ | 3,229 | $ | 2,989 | |||||

| Income from continuing operations |

$ | 346 | $ | 414 | $ | 390 | $ | 454 | $ | 343 | |||||

| Income from discontinued operations |

223 | 25 | 60 | 62 | 35 | ||||||||||

| Net income |

$ | 569 | $ | 439 | $ | 450 | $ | 516 | $ | 378 | |||||

| Net income per share—basic: |

|||||||||||||||

| Continuing operations |

$ | 2.14 | $ | 2.48 | $ | 2.23 | $ | 2.40 | $ | 1.76 | |||||

| Discontinued operations |

1.37 | 0.15 | 0.34 | 0.33 | 0.18 | ||||||||||

| Total |

$ | 3.51 | $ | 2.64 | $ | 2.57 | $ | 2.74 | $ | 1.94 | |||||

| Net income per share—diluted: |

|||||||||||||||

| Continuing operations |

$ | 2.12 | $ | 2.45 | $ | 2.20 | $ | 2.38 | $ | 1.74 | |||||

| Discontinued operations |

1.36 | 0.15 | 0.34 | 0.33 | 0.17 | ||||||||||

| Total |

$ | 3.49 | $ | 2.60 | $ | 2.53 | $ | 2.70 | $ | 1.91 | |||||

| Total assets |

$ | 9,331 | $ | 11,846 | $ | 6,252 | $ | 6,092 | $ | 8,383 | |||||

| Long-term debt (including current maturities) |

4,105 | 5,405 | 745 | 595 | 505 | ||||||||||

| Shareholders’ equity |

2,594 | 2,467 | 2,426 | 2,466 | 2,564 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview